28k After Tax UK: Complete Guide To Monthly Take-Home Pay, Taxes, Pensions, And Student Loans

On a £28,000 salary, take-home pay in the UK is £23,680 per year, £1,973 per month, and £455 per week for the 2025/26 tax year. These figures assume tax code 1257L, PAYE employment, and standard rates for England, Wales, and Northern Ireland.

Pension contributions and student loan repayments alter this figure depending on individual circumstances.

Key Takeaways

- A £28,000 gross salary produces £23,680 in annual net pay after HMRC deductions of £3,086 in income tax and £1,234 in National Insurance for 2025/26.

- Auto-enrolment pension contributions reduce monthly take-home from £1,973 to approximately £1,883, while the employer adds a further £54 per month to the pension pot.

- Plan 2 student loan holders, the most common group, pay no repayment deduction on £28,000, as the salary falls below the £29,385 repayment threshold.

What Is 28k After Tax in the UK?

A £28,000 gross salary becomes £23,680 in annual take-home pay once HMRC applies income tax and National Insurance deductions under the standard PAYE system. That translates to £1,973 per month and £455 per week, assuming tax code 1257L and no additional deductions.

Income tax on £28,000 is calculated under the Income Tax Act 2007. The Personal Allowance of £12,570 is deducted first, leaving taxable income of £15,430.

The basic rate of 20% applies to that taxable amount in full, producing an income tax liability of £3,086 per year.

The full taxable amount of £15,430 falls within the basic rate band, with no higher rate liability at this salary level.

Tax code 1257L is the standard code assigned to most employees with one job and no untaxed income. A non-standard code can meaningfully alter take-home pay on a £28,000 salary, sometimes by several hundred pounds per year.

A code lower than 1257L means HMRC is collecting additional tax, reducing net pay below £1,973 per month. If a payslip does not reflect the expected figure, checking the tax code directly with HMRC is the fastest way to identify the discrepancy.

How National Insurance Affects Your Take-Home Pay on 28,000?

National Insurance on a £28,000 salary costs £1,234 per year, or approximately £103 per month. Contributions begin above the primary threshold of £12,570, and the employee rate of 8% applies to all earnings between that threshold and the upper earnings limit of £50,270.

On £28,000, the NI calculation applies 8% to £15,430 of earnings, producing the £1,234 annual figure. Some older salary calculator pages still display a National Insurance figure of £1,543 for a £28,000 salary.

That reflects a previous rate before the reduction introduced from January 2024 onward. The correct figure, confirmed via HMRC guidance, is £1,234 for 2025/26.

Combined, income tax and National Insurance reduce £28,000 gross to £23,680 net. Pension contributions and student loan repayments apply on top of that figure and vary by individual circumstances.

| Deduction | Annual | Monthly | Weekly |

|---|---|---|---|

| Gross salary | £28,000 | £2,333 | £538 |

| Income tax | £3,086 | £257 | £59 |

| National Insurance | £1,234 | £103 | £24 |

| Take-home pay | £23,680 | £1,973 | £455 |

Figures confirmed for 2025/26 via HMRC. Tax code 1257L, PAYE, England, Wales, and Northern Ireland assumed.

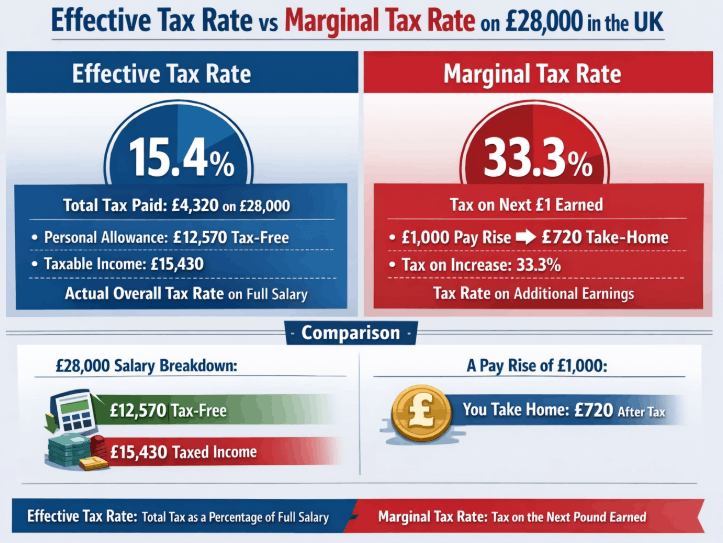

Effective Tax Rate vs Marginal Tax Rate on 28,000

The effective tax rate on a £28,000 salary is approximately 15.4%. The marginal tax rate shown on most calculator pages is 33.3%.

These two figures measure different things, and treating them as interchangeable produces a distorted picture of what a £28,000 salary actually costs in tax.

On a £28,000 salary, the effective tax rate is approximately 15.4%, meaning the combined income tax and National Insurance bill amounts to roughly £4,320 on £28,000 of gross earnings.

The marginal rate of 33.3% applies only to the next pound earned above current income. It does not apply to the entire salary.

The effective rate is lower because the Personal Allowance shelters the first £12,570 from both income tax and National Insurance.

Only £15,430 is taxable. A marginal rate printed on a calculator page tells a prospective employee what percentage of a pay rise will go to HMRC, not what percentage of the current salary is lost to tax.

A £1,000 pay rise on a £28,000 salary yields approximately £720 in additional take-home after combined income tax and NI at the basic rate.

The gap widens considerably at higher earnings, someone on 50k after tax sees a different marginal and effective rate picture once earnings cross the higher rate threshold at £50,270.

Turning down a pay rise on the assumption that a third of it disappears to HMRC misreads what the marginal rate actually measures. At £28,000, the entire salary remains within the basic rate band, so no additional rate applies to a modest pay increase.

How Pension Contributions Change Your 28,000 Take-Home?

Auto-enrolment under the Pensions Act 2008 reduces monthly take-home from £1,973 to approximately £1,883 at minimum contribution rates. The employer contributes a further £54 per month, making the pension deduction less costly than the payslip figure alone suggests.

The qualifying earnings band is the part of the pension calculation that rarely appears on a payslip or in standard employer guidance.

Under rules set by The Pensions Regulator, pension contributions are calculated on earnings between £6,240 and £50,270, not on the full gross salary. On £28,000, that produces qualifying earnings of £21,760.

How auto-enrolment pension deductions are calculated on a £28,000 salary:

- Subtract the lower qualifying earnings threshold from gross salary: £28,000 minus £6,240 equals £21,760 in qualifying earnings.

- Apply the minimum employee contribution rate of 5%: 5% of £21,760 equals £1,088 per year, or £91 per month.

- Apply the minimum employer contribution rate of 3%: 3% of £21,760 equals £653 per year, approximately £54 per month.

- Deduct the employee contribution from net take-home: £23,680 minus £1,088 equals £22,592 annually, or £1,883 per month.

- Add the employer contribution to assess total pension value: £1,088 plus £653 equals £1,741 in combined annual pension contributions.

Salary sacrifice arrangements, where available, allow employees to contribute to their pension before income tax and National Insurance are applied to their gross pay.

On £28,000, a 5% salary sacrifice contribution reduces the taxable pay figure, which lowers both the income tax and NI calculation compared with a standard relief at source arrangement.

The tax efficiency of salary sacrifice becomes significantly more pronounced at higher income levels, where the higher rate band applies, as the figures for £80,000 after tax illustrate.

Student Loan Deductions on a 28,000 Salary

Student loan deductions on a £28,000 salary depend entirely on which repayment plan applies.

Under Plan 2, the most widely held plan for graduates who started university in England after 2012, no deduction applies at £28,000 because the salary sits below the £29,385 annual repayment threshold set by the Student Loans Company.

Plan 1 holders face a small deduction. The Plan 1 threshold stands at £26,900 for 2025/26, so repayments of 9% apply to earnings above that figure. On £28,000, the difference is £1,100, producing an annual repayment of £99, or approximately £8 per month.

| Loan Plan | Annual Threshold | Monthly Deduction | Monthly Take-Home |

|---|---|---|---|

| No student loan | N/A | £0 | £1,973 |

| Plan 1 (pre-2012) | £26,900 | £8 | £1,965 |

| Plan 2 (post-2012) | £29,385 | £0 | £1,973 |

| Plan 4 (Scotland) | £33,795 | £0 | £1,973 |

| Postgraduate Loan | £21,000 | £35 | £1,938 |

Figures based on 2025/26 thresholds per HMRC and Student Loans Company guidance.

Postgraduate Loan repayments apply at 6% above the £21,000 threshold. On £28,000, that produces a deduction of approximately £420 per year, or £35 per month.

Repayments for all plans are collected through PAYE automatically by HMRC, requiring no separate action from the employee.

What Is 28k After Tax in Scotland?

Scottish taxpayers on a £28,000 salary pay marginally less income tax than equivalent earners in England, Wales, and Northern Ireland under 2025/26 rates.

The reason is that part of the taxable income falls into the Scottish starter rate of 19%, which is lower than the 20% basic rate applied across the rest of the UK.

The Scottish Government sets income tax rates and bands independently for earned income.

For 2025/26, the Scottish starter rate of 19% applies to income between £12,571 and £15,397. The basic rate of 20% covers income from £15,398 to £27,491. Above £27,492, the intermediate rate of 21% applies up to £43,662.

On £28,000, approximately £509 of income sits within the 21% intermediate band, partially offsetting the starter rate benefit lower down.

Employee National Insurance is calculated under UK-wide rules regardless of where an employee lives.

A Scottish taxpayer on £28,000 pays the same NI as an equivalent earner in England. The net effect is a take-home figure marginally above the England, Wales, and Northern Ireland baseline.

Scottish income tax rules apply based on where an employee lives, not where their employer is based.

Is 28,000 a Good Salary in the UK?

A £28,000 salary sits below the median for full-time UK employees. The Office for National Statistics Annual Survey of Hours and Earnings recorded a full-time median of £39,039 for April 2025, with the all-employee median at £32,890 once part-time workers are included.

A salary closer to that full-time median, such as £38,000 after tax, produces a noticeably different monthly figure and a more comfortable margin against average UK rents.

At £28,000, take-home pay of £1,973 per month sits above the National Living Wage full-time equivalent but falls short of the ONS full-time median of £39,039 recorded for April 2025.

For most professional roles, location determines whether that monthly figure is workable. What £1,973 per month means in practical terms varies sharply by region:

- Average UK rent outside London stood at approximately £1,200 per month in 2025, leaving roughly £773 for all remaining outgoings, including bills, food, and transport.

- The National Living Wage full-time equivalent at £12.21 per hour for 2025/26 produces a gross annual salary of approximately £25,397, placing £28,000 above the minimum wage floor but well short of the national median.

- ONS ASHE data shows the hospitality and retail sector median for full-time employees in 2025 was approximately £28,687, placing £28,000 at the lower end of typical pay in those sectors.

- The recommended rent affordability ceiling of 30% of monthly take-home on £1,973 is approximately £592, a figure below average rents in most UK cities outside the North and Midlands.

The gap between workable and stretched on £1,973 a month is largely a question of where in the UK someone lives. In lower-cost regions such as the North East, Northern Ireland, and parts of Wales, a monthly take-home of £1,973 is workable for a single person.

In London and the South East, where average rents regularly exceed £1,500 per month, the same figure requires shared accommodation or additional income to cover basic costs.

Conclusion

A £28,000 gross salary delivers £23,680 in annual take-home pay for 2025/26 under standard PAYE conditions. Pension contributions, student loan plans, tax code variations, and location all determine what that figure means in practice.

Tax codes, thresholds, and contribution rates change with each Budget, so checking current figures directly on GOV.UK ensures any calculations reflect the latest position. A 28k after tax income means £1,973 per month for most UK employees in 2025/26.

FAQ

How Much Is 28k a Month After Tax

£28,000 per year produces a monthly take-home pay of £1,973 under standard 2025/26 PAYE assumptions with tax code 1257L and no pension or student loan deductions.

How Much National Insurance Do You Pay on 28,000

National Insurance on a £28,000 salary is £1,234 per year, or £103 per month, for 2025/26. The 8% employee rate applies to earnings above the £12,570 primary threshold up to the upper earnings limit.

What Is the Hourly Rate for a 28,000 Salary

A £28,000 salary equates to approximately £11.38 per hour after tax, based on a standard 40-hour week and 52 weeks. At 37.5 hours per week, the after-tax hourly rate rises to approximately £12.14.

How Much Income Tax Do You Pay on 28,000

Income tax on a £28,000 salary is £3,086 per year, or £257 per month, for 2025/26. The full taxable income of £15,430, after the Personal Allowance is applied, falls within the 20% basic rate band with no higher rate liability.

Disclaimer: This article provides general financial information based on 2025/26 UK tax rates; for personalized financial advice or tax code disputes, please consult HMRC or a certified financial advisor.