Tax Code BR Meaning: Why You Are Overpaying Tax on a Main Job and How to Fix It With HMRC

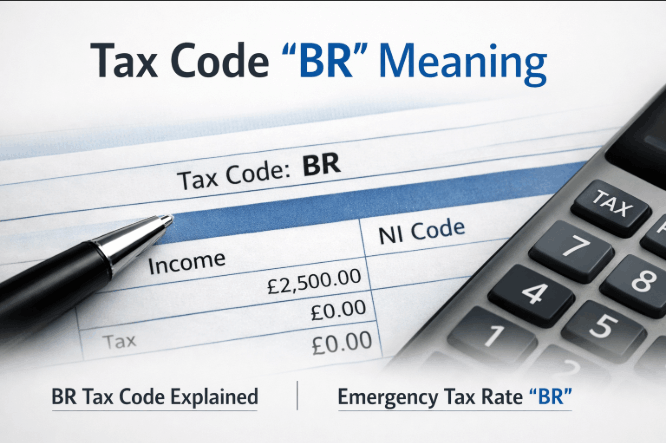

Tax code BR stands for Basic Rate. Under the UK’s Pay As You Earn (PAYE) scheme, HM Revenue & Customs (HMRC) uses it to instruct employers to deduct income tax at 20% on every pound earned from a specific income source, with no personal allowance of £12,570 applied, as confirmed by HMRC for the 2025/26 tax year.

Key Takeaways

- Tax code BR means all income from that source is taxed at 20% with no personal allowance offset, costing a basic-rate taxpayer on a £28,000 salary approximately £2,514 more per year than the standard 1257L code.

- BR is the correct code for a second job or additional pension where the £12,570 personal allowance is already used by a main income source; applied to a sole or main employment, it signals overpayment.

- Overpaid tax caused by an incorrect BR code can be reclaimed for the current tax year plus the four previous tax years, the claim must be initiated by the taxpayer, not HMRC.

What Does Tax Code BR Mean?

Tax code BR means Basic Rate. Every pound of income from that employment or pension is taxed at 20% under the PAYE scheme, with no personal allowance applied at that source.

Under the Income Tax (Earnings and Pensions) Act 2003, HMRC instructs employers to calculate income tax using a tax code for every PAYE employee.

The standard code 1257L in 2025/26 applies the £12,570 personal allowance, meaning no income tax is due on the first £12,570 of earnings from that source. Tax code BR removes that buffer entirely. From the first pound earned in that role or pension, 20% income tax is deducted.

From the first pound earned in that role or pension, 20% income tax is deducted, and in the right circumstances, that is exactly what should happen.

BR is not technically an emergency tax code. Emergency codes carry a W1, M1, or X suffix, indicating non-cumulative taxation.

BR can act as a temporary measure when HMRC lacks income information, but for a second job or pension, it is permanent and correct. The distinction matters, BR on a second job is permanent and correct, not a system error requiring urgent resolution.

Whether BR is right or wrong depends entirely on how many income sources exist and where the personal allowance currently sits.

Why Has a Tax Code Been Set to BR?

HMRC assigns tax code BR when the personal allowance is already allocated elsewhere, or when it does not hold sufficient information about an employee’s income situation.

Four situations most commonly trigger BR assignment:

- Second employment: A main job uses the full £12,570 personal allowance under code 1257L, so any additional employment defaults to BR on that second income source

- Pension alongside employment: Where employment already uses the personal allowance, a pension provider correctly applies BR to the pension payments

- New job without a P45: Without a P45 from a previous employer, HMRC cannot confirm prior earnings or allowance use and applies BR as a precautionary default

- Starter Checklist Statement C: When starting a new role, employees complete an HMRC Starter Checklist; selecting Statement C (“I have another job or pension”) directly triggers BR on the new income source

That final point is the most overlooked cause of an incorrect BR code. Selecting the wrong Starter Checklist statement, choosing Statement B when Statement C is correct, or vice versa, misdirects HMRC’s PAYE system immediately.

Statement B tells HMRC this is the main employment; Statement C tells it a second income exists elsewhere. A wrong selection cannot self-correct. It requires a direct update to HMRC to resolve, and the resulting overpayment accumulates with every payroll run until that contact is made.

The trigger matters, it is the clearest indicator of whether the code is right or whether a correction is needed.

BR Tax Code vs 1257L: What Is the Difference?

The difference between BR and 1257L comes down to the personal allowance. Code 1257L applies the full £12,570 tax-free threshold; BR applies none.

On a £28,000 salary, that gap produces approximately £2,514 in additional tax per year.

| Feature | Tax Code BR | Tax Code 1257L |

|---|---|---|

| Personal Allowance applied | £0 | £12,570 |

| Tax rate applied | 20% on all income | 20% above £12,570 only |

| Typical use | Second job, additional pension | Main or only employment |

| Cumulative? | Yes | Yes |

| Approx. take-home on £28,000 | £22,400 | £24,914 |

Based on 2025/26 income tax rates, England, Wales, and Northern Ireland. National Insurance calculated separately.

Sole traders drawing both self-employed and PAYE income have more than one tax threshold to keep in order, the VAT threshold 2025 sits alongside PAYE code accuracy as a separate but equally important compliance checkpoint.

If BR is showing against a main or only employment, the £2,514 annual difference in the table makes the cost of inaction clear.

BR Tax Code on a Second Job or Pension: When It Is Correct

BR is the correct code when a main income source already holds the full personal allowance. Taxing the second source at 20% from pound one produces the same total annual tax liability as if all income came from a single employer, the split changes the timing of deduction, not the total amount owed.

Three situations where BR is the right code:

- A main employed position carries code 1257L using the full £12,570 allowance, any additional employed position correctly carries BR on that second income

- A workplace or private pension is received alongside employment income, the pension provider correctly applies BR to pension payments where employment already holds the personal allowance

- A one-off PAYE engagement or freelance payment sits alongside a main employment, BR correctly applies to that standalone payment

Where combined income across both sources exceeds £50,270 in 2025/26, HMRC replaces BR with D0, applying the 40% higher rate to the second source. Those with multiple income streams may also need to register for Self Assessment depending on total earnings.

When BR is correctly applied, no additional tax is paid, the liability is identical to a single employment; it is simply collected differently.

When BR Is Wrong and What It Costs?

An incorrect BR code applied to a main employment wastes the full £12,570 personal allowance.

For a basic-rate taxpayer on a £28,000 salary, that amounts to approximately £2,514 in overpaid income tax for the year, rising to over £5,000 if left uncorrected across two tax years.

The most common route to this error is completing the wrong statement on the HMRC Starter Checklist at the start of a new job. Selecting Statement C when the role is actually a main employment, not a second job, triggers BR on income that should carry 1257L from day one.

Dynamic Coding creates a second route to the same problem. HMRC expanded this system in 2025 to adjust tax codes mid-year using real-time income data.

An employee whose code shifts unexpectedly, sometimes to a reduced-allowance code or to BR between payroll runs, may find the next payslip deducting significantly more tax than expected, with no prior notification.

Dynamic Coding is HMRC’s system for adjusting PAYE tax codes mid-year based on real-time income data, expanded in 2025.

Where HMRC receives information indicating additional income, such as a second PAYE engagement or a one-off payment, it can reassign or alter a code between payroll runs.

This can result in BR being applied without prior notification to the employee, increasing the monthly tax deduction immediately.

The financial cost of an incorrect BR code compounds with every pay period, the sooner it is identified, the smaller the overpayment to reclaim.

How to Fix a BR Tax Code: Step-by-Step

Correcting an incorrect BR code requires one contact with HMRC, via the Personal Tax Account online or by telephone. The revised code is issued directly to the employer and takes effect from the next payroll run.

Follow these steps in order:

- Locate the current tax code: It appears on every payslip near the National Insurance number, on the P60 issued at tax year end, and within the HMRC Personal Tax Account at gov.uk

- Confirm whether BR is correct: If it applies to a second job or pension where the main income holds 1257L, no action is needed; if it applies to a main or only job, a correction is required

- Log into the Personal Tax Account: At gov.uk/personal-tax-account to update income details and request a code review, the fastest route, available around the clock

- Call the HMRC income tax helpline on 0300 200 3300 (Monday to Friday, 8 am–6 pm): Have the National Insurance number and the employer’s PAYE reference from the payslip ready before calling

- HMRC issues a revised coding notice (P2): Directly to the employer, the corrected code applies from the next payroll run, and any in-year overpayment is typically refunded through payroll automatically

Contractors starting a new PAYE engagement, where BR may initially apply, can also run a VAT number check by company name to confirm the new employer’s registered status before the first payroll run.

Where BR has run incorrectly for more than one pay period, the section below covers what can be reclaimed and how far back the claim can reach.

How to Claim Back Overpaid Tax on a BR Code?

Overpaid income tax caused by an incorrect BR code is reclaimable for the current tax year and the four previous tax years, with a maximum look-back of five tax years from the point of claim.

Three routes are available:

- In-year employer adjustment: Once HMRC corrects the code during the active tax year, the employer refunds the overpayment automatically through the next payroll run

- P800 tax calculation notice: HMRC issues a P800 between June and November following the end of the relevant tax year, stating the overpayment amount and how to claim online (typically within five working days) or by cheque

- Direct Personal Tax Account claim: Where no P800 arrives but overpayment is believed to exist, a repayment claim can be submitted directly through the Personal Tax Account at gov.uk

The statutory time limit for reclaiming overpaid PAYE income tax, including tax overpaid under an incorrect BR code, is four years from the end of the relevant tax year, under UK tax law.

For overpayments made in 2021/22, the claim deadline is 5 April 2026. HMRC does not extend this deadline; overpayments unclaimed after it expires are not returned.

Waiting for HMRC to make contact is not a reliable strategy, the claim must come from the taxpayer’s side.

SBR Tax Code: The Scottish Equivalent of BR

SBR is Scotland’s equivalent of the BR tax code. It appears on a second job or additional pension for Scottish taxpayers, applying the Scottish Rate of Income Tax (SRIT) to that income source with no personal allowance applied.

The S prefix on any HMRC tax code signals that Scottish income tax rates apply. Scottish taxpayers pay income tax across a different band structure, administered by HMRC but set under SRIT by the Scottish Government.

At the basic rate band, the Scottish rate is also 20%, so the immediate cash impact of SBR is identical to BR for most earners.

The distinction matters for payroll accuracy and higher-rate scenarios. According to HMRC, employers must apply the tax code exactly as issued, using the correct regional prefix is not discretionary.

An employer applying standard BR to a Scottish employee’s second income source is using the wrong code, even if the deducted amount is currently identical.

Where SBR appears on a sole or main income source, the same fix process applies, contact HMRC via the Personal Tax Account or by calling the income tax helpline.

Conclusion

Tax code BR means Basic Rate, 20% income tax on every pound from that income source, with no personal allowance applied. For second jobs and pensions, it is correct.

On a main employment, it costs roughly £2,514 per year in overpaid tax. One contact with HMRC fixes it, and the statutory four-year reclaim window keeps past overpayments fully recoverable for UK PAYE taxpayers in 2025/26.

FAQ

Is BR an emergency tax code?

No, not technically. Emergency codes carry a W1, M1, or X suffix. BR can act as a temporary measure when HMRC lacks income data, but applied to a second job or pension, it is a permanent and correct code, not an emergency assignment.

What does BR mean on a payslip?

The tax code BR meaning is Basic Rate: all income from that source is taxed at 20% with no personal allowance applied. It is correct for second jobs and pensions, but indicates an error on a sole or main employment.

Can the personal allowance be split between two jobs?

Yes. HMRC allows the £12,570 personal allowance to be divided between two employers. Contact HMRC directly to request the split. Each employer receives a revised coding notice. This avoids BR on a second job where combined earnings stay within the personal allowance.

How long does HMRC take to correct a BR tax code?

HMRC typically issues a corrected code within a few working days of being contacted. The employer applies it from the next payroll run. Where the tax year has already ended, a P800 notice arrives between June and November with the overpayment figure.

Does BR affect National Insurance contributions?

No. National Insurance is calculated independently of PAYE tax codes. BR affects only the income tax deduction from a specific source, NI thresholds and rates apply to gross earnings regardless of whether the tax code is BR, 1257L, or any other code.

Disclaimer: This article is for informational purposes only and does not constitute formal financial or legal advice; always verify your tax status directly with HMRC.