38k After Tax: Full UK Salary Breakdown, Deductions, Regional Variations, And Net Take-Home

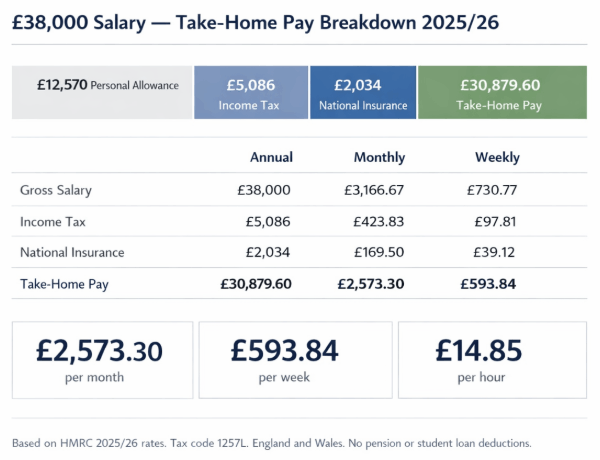

On a gross salary of £38,000, a standard PAYE employee in England or Wales takes home £30,879.60 per year after Income Tax and National Insurance in the 2025/26 tax year. That works out to £2,573.30 per month, £593.84 per week, and £14.85 per hour based on a 40-hour week.

The effective tax rate is 18.74%, confirmed against current HMRC rates under tax code 1257L.

Key Takeaways

- Annual take-home on £38,000 is £30,879.60 for the 2025/26 tax year: Based on tax code 1257L, PAYE employment in England or Wales, with no student loan and no pension deduction.

- Total deductions amount to £7,120.40: Comprising £5,086.00 in Income Tax at the 20% basic rate and £2,034.40 in National Insurance Class 1 contributions.

- Scottish earners on the same salary take home approximately £30,521.60: Around £358 less annually, because the Scottish Government applies its own intermediate income tax rate of 21% above £14,876.

- The Personal Allowance has been frozen at £12,570 since the 2021/22 tax year: Legislatively confirmed to stay frozen until at least April 2028 under the Finance Acts, creating a real-terms tax increase for anyone whose pay rises.

- A Plan 2 student loan reduces monthly take-home by £80.29: Bringing the net monthly figure down to approximately £2,493 for the majority of graduates who started courses after August 2012.

How Much Is £38,000 After Tax Per Month in the UK?

The monthly take-home pay on a £38,000 salary is £2,573.30 in 2025/26, the figure most people need for budgeting, mortgage applications, and rent affordability checks. That assumes standard tax code 1257L, PAYE employment, no pension contributions, and no student loans. Each variable is covered in full below.

| Annual | Monthly | Weekly | |

|---|---|---|---|

| Gross Salary | £38,000.00 | £3,166.67 | £730.77 |

| Personal Allowance (0%) | £12,570.00 | £1,047.50 | £241.73 |

| Taxable Income | £25,430.00 | £2,119.17 | £489.04 |

| Income Tax (20%) | £5,086.00 | £423.83 | £97.81 |

| National Insurance (8%) | £2,034.40 | £169.53 | £39.12 |

| Take-Home Pay | £30,879.60 | £2,573.30 | £593.84 |

Source: HMRC 2025/26 confirmed rates. Basis: tax code 1257L, England/Wales, PAYE employment, no pension, no student loan.

Effective Tax Rate

The effective tax rate on a £38,000 salary is 18.74% in 2025/26, meaning 18.74p of every pound earned goes to HMRC in combined Income Tax and National Insurance.

This is materially lower than the headline 20% basic rate because the Personal Allowance shields the first £12,570 from any tax at all. For mortgage and lending purposes, lenders assess net income of £30,879.60 rather than the gross £38,000 figure.

The weekly figure of £593.84 is the annual net pay divided by 52. Most employees receive monthly payslips, so the £2,573.30 monthly figure is what actually lands in a bank account.

For salaried workers mapping out their household budgets, it is equally helpful to align financial planning with the calendar year, particularly when factoring in time off around the upcoming UK Bank Holidays 2026 schedule. This ensures that both mandatory deductions and planned leisure time are accounted for well in advance.

The daily and hourly breakdowns, £118.77 per day and £14.85 per hour at 40 hours per week, matter most for freelancers and contractors comparing their day rate against a permanent equivalent.

For those operating as sole traders or independent contractors, managing overheads is just as critical as tracking net income, which often includes sourcing the best card reader for small business transactions to keep processing fees low.

Understanding these precise take-home figures helps independent professionals price their services accurately to cover both personal taxes and operational expenses.

How Income Tax and National Insurance Are Calculated on £38,000?

PAYE calculates Income Tax and National Insurance separately, using different thresholds but the same gross salary as the starting point. The sequence HMRC follows is the same for every PAYE employee on this salary.

- HMRC assigns tax code 1257L: This confirms a tax-free Personal Allowance of £12,570 for the year. A different code changes the allowance and, therefore, the net pay.

- Taxable income is established: £38,000 minus £12,570 leaves £25,430 subject to Income Tax.

- The basic rate of 20% is applied to the full £25,430, producing an annual Income Tax liability of £5,086.00. The entire taxable portion sits within the basic rate band, which runs to £50,270. No higher-rate tax applies at this salary.

- National Insurance Class 1 is calculated at 8%: On earnings between £12,570 and £50,270. On £38,000, this produces an annual NI contribution of £2,034.40.

- Both deductions are divided by 12: To produce the monthly payslip figures: £423.83 Income Tax and £169.53 National Insurance.

- Net pay is confirmed: £38,000 minus £5,086.00 minus £2,034.40 equals £30,879.60 annually, or £2,573.30 per month.

A £38,000 salary sits comfortably within the basic rate band, there is no higher-rate tax until gross earnings exceed £50,270. For all Income Tax purposes, including savings interest and dividends, HMRC treats a £38,000 earner as a basic rate taxpayer.

What Does the Effective Tax Rate Actually Mean on a £38,000 Salary?

The effective tax rate on 38k after tax is 18.74%, not 20%. The marginal rate only applies to taxable income above £12,570. Because the Personal Allowance shelters a significant portion of a £38,000 salary, the true burden across the whole income is lower than the headline figure suggests.

The Low Incomes Tax Reform Group (LITRG) consistently highlights the effective rate as the figure that reflects real-world tax burden rather than the marginal rate politicians typically reference.

For someone on £38,000, a combined Income Tax and NI effective rate of 18.74% means keeping 81.26p of every pound earned.

Mortgage affordability is where this distinction matters most. Lenders apply their multipliers to net income, not gross.

A standard 4.5x multiplier applied to £30,879.60 gives a maximum loan estimate of approximately £138,958, meaningfully lower than the £171,000 a 4.5x gross calculation would produce.

The Frozen Personal Allowance and What It Costs a £38,000 Earner

The Personal Allowance has been fixed at £12,570 since 2021/22 and is legislatively confirmed to remain there until at least April 2028 under successive Finance Acts.

The House of Commons Library has documented this as fiscal drag, as wages rise with inflation, a larger share of income enters the taxable band without any change to the headline rate.

What Does the Freeze Mean in Practice?

Had the Personal Allowance risen with CPI inflation since 2021/22, it would sit at approximately £14,600 by 2025/26. For a £38,000 earner, that frozen difference of £2,030 taxed at 20% represents £406 paid to HMRC annually, which would not be due under an inflation-linked threshold.

The House of Commons Library estimates the freeze will generate an additional £25 billion in annual tax receipts by 2027/28.

A 4% pay rise from £38,000 to £39,520 produces £1,520 in additional gross income. All £1,520 is fully taxable, generating an extra £304 in Income Tax and £121.60 in NI.

Net pay rises by £1,094.40 rather than the £1,520 the gross figure implies. The freeze applies in England, Wales, and Northern Ireland. Scotland sets its own thresholds under devolved powers.

- Every pay rise above inflation increases the effective tax rate, not because rates have changed, but because the threshold has not moved.

- Workers moving from £38,000 toward £40,000 over the next two to three years will cross threshold territory more quickly than in any previous decade.

- The freeze disproportionately affects earners in the £30,000 to £50,000 range, those whose entire taxable income sits in the basic rate band with no higher-rate reliefs to offset it.

- Salary sacrifice pension contributions become a more effective tool under a frozen threshold because they reduce gross pay and therefore reduce the amount of income pulled into the taxable band.

£38,000 After Tax in Scotland: A Different Take-Home Figure

A £38,000 earner in Scotland takes home less than an equivalent earner in England or Wales. The Scottish Government sets its own income tax rates and bands under devolved powers, and its structure diverges from the rest of the UK above the starter rate threshold.

National Insurance contributions are identical across all four nations; only Income Tax differs.

In 2025/26, Scottish income tax applies a 19% starter rate up to £14,876, a 20% basic rate between £14,876 and £26,561, and a 21% intermediate rate between £26,561 and £43,662.

A £38,000 earner falls into the intermediate rate band for a portion of their taxable income, resulting in a higher overall Income Tax bill than an England or Wales equivalent.

| England / Wales | Scotland | |

|---|---|---|

| Income Tax Paid | £5,086.00 | approx. £5,444.00 |

| National Insurance | £2,034.40 | £2,034.40 |

| Annual Take-Home | £30,879.60 | approx. £30,521.60 |

| Monthly Take-Home | £2,573.30 | approx. £2,543.47 |

Scotland figures based on 2025/26 Scottish Government confirmed rates. Verify your exact figure via the Scottish Government’s income tax calculator at gov.scot.

The gap of approximately £358 annually, or around £29.83 per month, is worth factoring in when comparing job offers across the Scottish border. A role paying £38,000 in Edinburgh produces less net income than the same role in Manchester, Leeds, or Cardiff.

Scots earning in this range who receive even a modest pay rise of up to £40,000 will remain in the intermediate rate band and see a higher effective rate than their English counterparts on the equivalent salary.

How Student Loans and Pension Contributions Change Your Take-Home Pay?

The headline £2,573.30 monthly figure assumes no student loan repayments and no pension contributions. For the majority of employed graduates and most workers enrolled in a workplace pension, the real take-home is lower.

Both deductions are taken before net pay is calculated, neither reduces taxable income for Income Tax or NI purposes, except where pension contributions are made via salary sacrifice.

The Student Loan Company collects repayments via PAYE, and the deduction shows as a separate line on the payslip alongside Income Tax and NI. Which plan applies determines both the threshold and the monthly deduction:

- Plan 2 (most graduates from courses starting on or after 1 August 2012): repayments at 9% on earnings above £27,295. On a £38,000 salary, this means 9% of £10,705, producing annual repayments of £963.45 and a monthly deduction of £80.29. Take-home falls to approximately £29,916.15 annually, or £2,493.01 monthly.

- Plan 1 (graduates from courses starting before 1 September 2012): threshold £24,990, repayments 9% on earnings above that. On £38,000, this produces annual repayments of £1,170.90 and a monthly deduction of £97.58. Take-home falls to approximately £29,708.70 annually, or £2,475.73 monthly.

- Plan 5 (students starting from August 2023 in England): threshold £25,000, same 9% rate above that. Annual repayments of approximately £1,170 on a £38,000 salary.

How pension contributions affect take-home pay depends on the arrangement your employer uses: salary sacrifice or standard relief-at-source.

Under auto-enrolment, the minimum employee contribution is 5% of qualifying earnings. For a £38,000 salary, that means approximately £1,900 annually diverted into the pension. Under salary sacrifice, this reduces your gross pay to £36,100, lowering both the Income Tax and NI calculation:

- Auto-enrolment minimum pension (5% salary sacrifice): annual take-home approximately £29,292, or £2,441 monthly. This is the most common pension scenario for employees on £38,000.

- Higher voluntary contribution (10% salary sacrifice): gross reduced to £34,200, annual take-home approximately £27,987, or £2,332 monthly. The tax and NI savings partially offset the contribution cost.

If you carry both a Plan 2 student loan and a minimum auto-enrolment pension, your actual monthly take-home on a £38,000 salary falls to approximately £2,413, over £160 less than the headline figure.

It is the most common deduction combination for graduate employees currently earning around this figure.

Is £38,000 a Good Salary in the UK?

A gross salary of £38,000 sits approximately 2.7% below the UK median for full-time employees. According to the Office for National Statistics Annual Survey of Hours and Earnings (ASHE), median gross annual earnings for full-time workers reached £39,039 in April 2025, placing £38,000 just below that midpoint but still comfortably above the earnings of the lower half of the working population.

Where you live changes that picture sharply:

- London: £38,000 falls well below the full-time median of approximately £46,000 (ONS ASHE 2025). After tax, £2,573.30 monthly covers rent in Zone 3 or 4 but leaves limited discretionary income in most borough areas.

- North East, North West, Wales, Yorkshire and the Humber: £38,000 sits above the regional full-time median. Net monthly pay of £2,573.30 provides real financial breathing room in lower-cost areas, particularly outside major city centres.

- South East outside London: £38,000 is competitive in many towns but stretched in commuter-belt areas where housing costs track closer to London levels.

- Scotland: the slightly lower net figure of approximately £2,543 still exceeds the Scottish full-time median of roughly £36,500 gross (ONS ASHE 2025).

On living standards, a single adult in the UK requires a net annual income of approximately £25,000 to meet the Resolution Foundation minimum income standard. The £30,879.60 take-home on a £38,000 salary exceeds that benchmark by nearly £6,000 annually for a single earner.

As a household income, £30,879.60 sits above the regional average across most of the UK outside London and the South East, based on ONS household income data.

The Bottom Line

The confirmed take-home on £38,000 for the 2025/26 tax year is £30,879.60 annually under standard HMRC conditions. Scotland, student loans, and pension contributions each reduce that figure in ways the headline number does not reflect.

For current figures specific to your tax code and deductions, the HMRC personal tax account at gov.uk gives the most accurate individual breakdown.

FAQ

What is £38,000 after tax as a weekly and hourly figure

The weekly take-home is £593.84, and the hourly rate is £14.85 at a standard 40-hour week. Figures are for the 2025/26 tax year, tax code 1257L, England and Wales, with no additional deductions.

How much National Insurance do you pay on £38,000

Class 1 NI on a £38,000 salary totals £2,034.40 annually, £169.53 per month. The 8% rate applies to earnings between £12,570 and £50,270. NI rates are identical across England, Scotland, Wales, and Northern Ireland; the contribution is not devolved.

What tax code applies to a £38,000 salary

The standard code is 1257L for most PAYE employees. If your payslip shows a different code, your take-home will differ from the figures in this article. Check and correct your tax code through your HMRC personal tax account at gov.uk/check-income-tax.

Does the £38,000 take-home figure change if you work part-time

Yes, part-time pay is calculated on the same pro-rata basis. The take-home is not simply a proportional share of £30,879.60 because the Personal Allowance still shelters the first £12,570 in full, producing a different effective rate at lower gross earnings.

How does £38,000 after tax compare to £40,000 after tax

A £40,000 salary produces approximately £32,279.60 annually, or £2,690 monthly. The £2,000 gross difference shrinks to around £1,400 net after the 28% combined Income Tax and NI deduction rate is applied to those additional earnings.

All figures confirmed against HMRC published rates for the 2025/26 tax year (6 April 2025 to 5 April 2026). Rates are subject to change. Verify current thresholds at gov.uk/income-tax-rates before making any financial decisions.